39 duration for zero coupon bond

Zero Coupon Bond Calculator - Nerd Counter How to Calculate the Price of Zero Coupon Bond? The particular formula that is used for calculating zero coupon bond price is given below: P (1+r)t; Examples: Now come to a zero coupon bond example, if the face value is $2000 and the interest rate is 20%, we will calculate the price of a zero coupon bond that matures in 10 years. How to Calculate Yield to Maturity of a Zero-Coupon Bond Oct 10, 2022 · Zero-Coupon Bond YTM Example . Consider a $1,000 zero-coupon bond that has two years until maturity. The bond is currently valued at $925, the price at which it could be purchased today. The ...

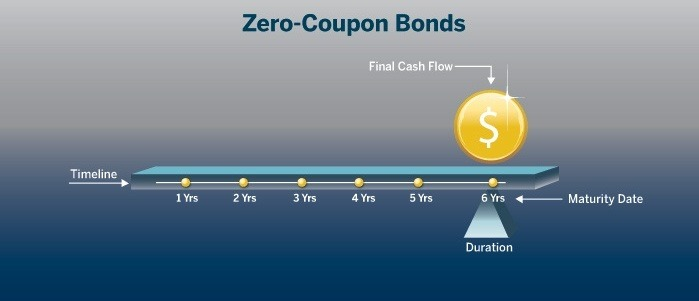

The Macaulay Duration of a Zero-Coupon Bond in Excel Aug 29, 2022 · The Macaulay duration of a zero-coupon bond is equal to the time to maturity of the bond. Simply put, it is a type of fixed-income security that does not pay interest on the principal amount.

Duration for zero coupon bond

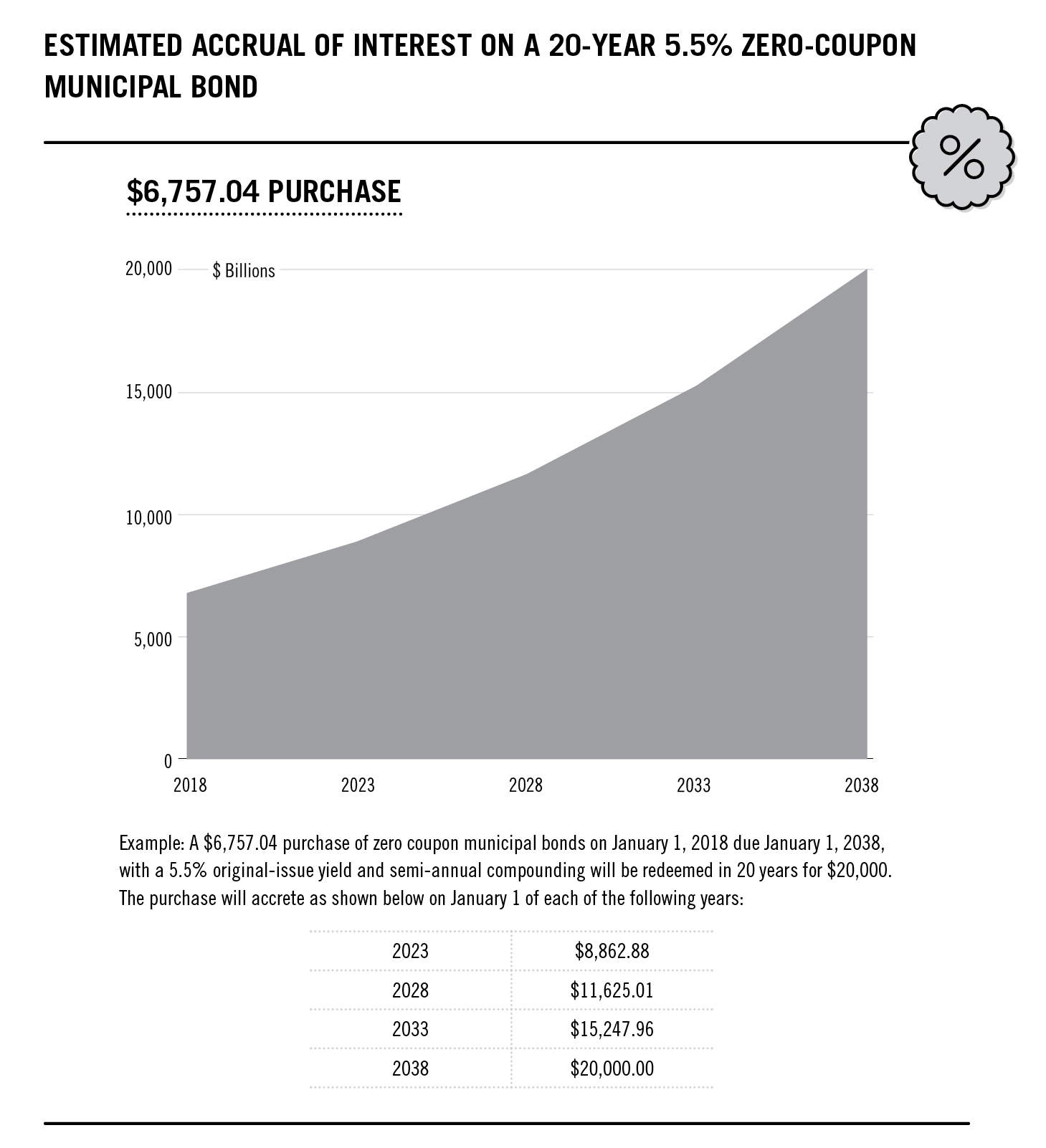

The One-Minute Guide to Zero Coupon Bonds | FINRA.org Oct 20, 2022 · For example, you might pay $3,500 to purchase a 20-year zero coupon bond with a face value of $10,000. After 20 years, the issuer of the bond pays you $10,000. For this reason, zero coupon bonds are often purchased to meet a future expense such as college costs or an anticipated expenditure in retirement. Advantages and Risks of Zero Coupon Treasury Bonds - Investopedia Jan 31, 2022 · If a zero-coupon bond is purchased for $1,000 and given away as a gift, the gift giver will have used only $1,000 of their yearly gift tax exclusion. ... Ext Duration Treasury ETF." PIMCO. "PIMCO ... Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond. Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield.

Duration for zero coupon bond. Bond duration: how it works and how you can use it - Monevator Oct 25, 2022 · What is bond duration? Bond duration expresses a bond’s vulnerability to interest rate risk. The larger the bond duration number, the more reactive a bond’s price is to interest rate changes, as the bond’s yield adjusts to reflect those changes. For example, if a bond’s duration number is 11, then it: Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond. Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield. Advantages and Risks of Zero Coupon Treasury Bonds - Investopedia Jan 31, 2022 · If a zero-coupon bond is purchased for $1,000 and given away as a gift, the gift giver will have used only $1,000 of their yearly gift tax exclusion. ... Ext Duration Treasury ETF." PIMCO. "PIMCO ... The One-Minute Guide to Zero Coupon Bonds | FINRA.org Oct 20, 2022 · For example, you might pay $3,500 to purchase a 20-year zero coupon bond with a face value of $10,000. After 20 years, the issuer of the bond pays you $10,000. For this reason, zero coupon bonds are often purchased to meet a future expense such as college costs or an anticipated expenditure in retirement.

Solved I. What is the Macaulay duration of a 5-year | Chegg.com

Bond Valuation and Risk - ppt video online download

Bond Price Volatility Zvi Wiener Based on Chapter 4 in ...

Zero Coupon Bond - QS Study

Problems 63–66 involve zero-coupon bonds. A zero-coupon bond is a bond that is sold now at a discount and will pay its face value at the time when it matures; no interest payments are made. ...

The Key To Duration: Sensitivity To Changing Interest Rates ...

Zero Coupon Bonds Explained (With Examples) - Fervent ...

Investor's Guide to Zero-Coupon Municipal Bonds | Project ...

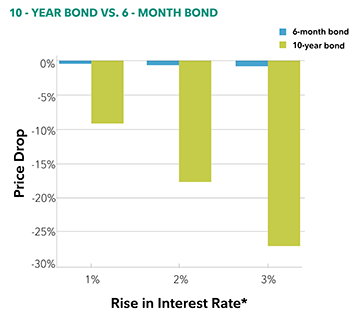

Under the Hood: What You Need to Know About Bond Duration and ...

Zero Coupon Bond Value - Formula (with Calculator)

Impossible Finance — The Perpetual Zero Coupon Bond | by ...

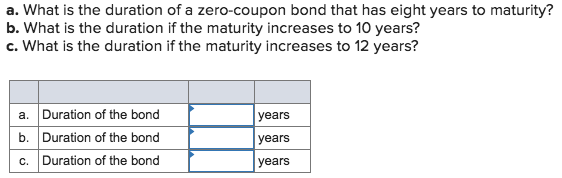

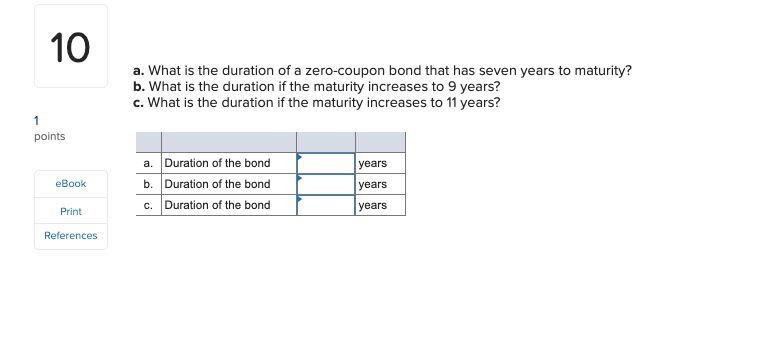

Solved a. What is the duration of a zero-coupon bond that ...

FRM: Dollar duration of zero coupon bond

:max_bytes(150000):strip_icc()/zero-couponbond_final-a6ec3618516a49c9a3654a1c79c9b681.png)

Zero-Coupon Bond: Definition, How It Works, and How To Calculate

Taylor Expansion To measure the price response to a small ...

Portfolio Duration and its Limitations | CFA Level 1 ...

Zero Coupon Bond Vs Regular Coupon Bond - Fintelligents

Zero-coupon bond - PrepNuggets

Invest in Zero Coupon Bond at Yubi | Learn All About It

Zero Coupon Bonds

How to Calculate PV of a Different Bond Type With Excel

Macaulay Duration

How to Calculate a Zero Coupon Bond Price | Double Entry ...

Solved] A 12.75-year maturity zero-coupon bond selling at a ...

SOLUTION: Duration of zero coupon bond - Studypool

Modified duration of zero-coupond bond (FRM practice question)

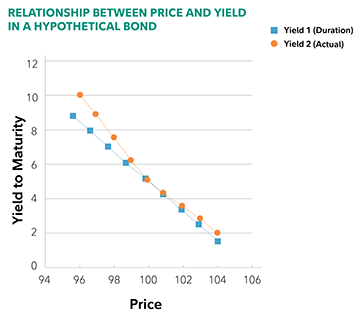

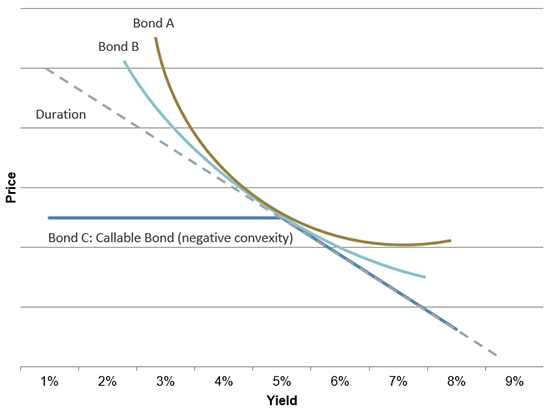

Duration: Understanding the Relationship Between Bond Prices ...

THE DURATION OF A BOND AS A PRICE ELASTICITY AND A FULCRUM

Duration & Convexity - Fixed Income Bond Basics | Raymond James

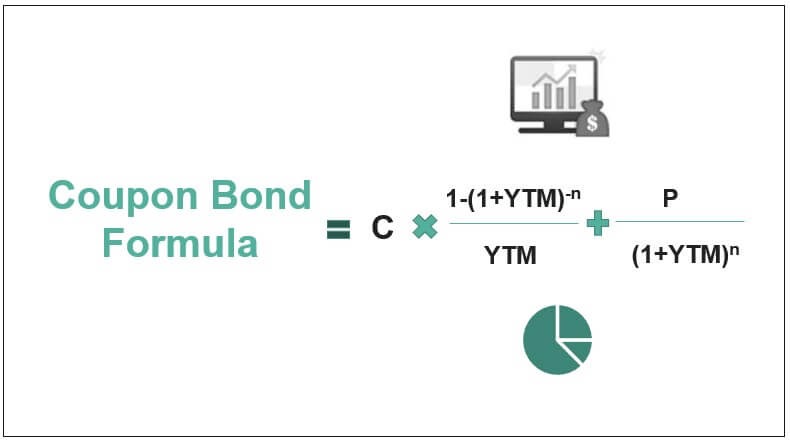

Coupon Bond Formula | How to Calculate the Price of Coupon Bond?

Duration and Zero Coupon Bonds - YouTube

Bond Fund Point of Indifference vs. Principle Recovery ...

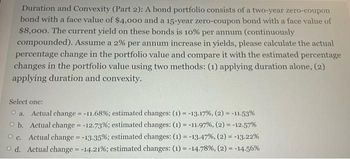

Answered: Duration and Convexity (Part 2): A bond… | bartleby

Solved a. What is the duration of a zero-coupon bond that ...

Solved] You are managing a portfolio of $1.3 million. Your ...

Duration: Understanding the Relationship Between Bond Prices ...

Zero Coupon Bond Introduction · Fixed Income

Zero Coupon Bond Calculator - Calculator Academy

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

Post a Comment for "39 duration for zero coupon bond"